“I have been following the absence of legal prosecutions since 2008, and have posted on that subject more than 500 times. But this isn’t the obsession of one lone crank (i.e., me). Many others in banking, law enforcement and government who aren’t on the payroll of banks have reviewed the events of the financial crisis and have reached the same conclusion — that the law was broken repeatedly by bankers.”

“Political access and lobbying go part way toward explaining the absence of prosecutions and, therefore, the lack of convictions…As we have repeatedly shown, Treasury Department officials, including former Treasury Secretary TimothyGeithner, had convinced prosecutors in the Justice Department of the dangers of prosecuting banks and bankers for the economy.” (Cartoon above via here.)

“People may have outrage fatigue about Wall Street, and more stories about billionaire greedheads getting away with more stealing often cease to amaze. But the HSBC case went miles beyond the usual paper-pushing, keypad-punching sort-of crime, committed by geeks in ties, normally associated with Wall Street. In this case, the bank literally got away with murder – well, aiding and abetting it, anyway.”

In Rolling Stone, Matt Taibbi explains how and why the Justice Department refused to prosecute HSBC for sundry violations of the law. In short, they were Too Big to Jail. “An arrestable class and an unarrestable class. We always suspected it, now it’s admitted. So what do we do?”

In related news, Wall Street bankers throw one of their customary hissyfits over a gaggle of fully complicit, bought-and-paid-for regulators finally being asked a hard question or two by the Senate Banking Committee — thanks to its and our new champion, Senator Elizabeth Warren. “The anonymous banker followed up [with Politico, naturally]: ‘Elizabeth Warren and Ted Cruz are dueling for the title of ‘most extreme fringe freshman senator.”

Anonymous Banker, let me choose my words carefully: Go fuck yourself. If this administration’s promises of change-we-can-believe-in were worth a dime, you and so many others would be doing hard time right about now.

Hey all. Apologies yet again for the lack of updates around here. As I said a couple oftimes last year, I’m still figuring out where the old Ghost fits in the scheme of life these days. There’s a negative feedback loop happening where I don’t post at GitM that often, so fewer people swing by here, so there are no comments or feedback on the posts that I do spend some time on, which makes me even less inclined to post, so thus even fewer people swing by here…you get the point.

I was thinking of starting up the movie reviews around here again for 2013, but having just spent a looong time on another giant project that few if any will ever peruse, I’m not really seeing the point of dedicating myself to spending even more hours of my day writing long-winded reviews that nobody ever reads. It’s just a lot of work with very little gain. I’ve been writing this blog for over 13 years and the reviews for over ten — If either were ever going to gain an audience, they would have done so by now.

I hate on the hipster Twitter kids, but establishment journalism is even worse. We live in a world where the totally inane Politicorules the roost and “wins the day”. Where our papers of record will keep warrantless wiretaps and drone bases quiet for years because the powers-that-be asked them to. Where idiot right-leaning “centrists” like David Brooks, David Gergen, Gloria Borger, and Cokie Roberts are queried for their inane views constantly, even though they don’t know anything and have never done anything with their lives but constantly mouth Beltway platitudes as if they were Holy Scripture. Where “journalists” like Chuck Todd, John King, and Jake Tapper — the latter of whom, let’s remember, made it big by kissing-and-telling on his Big Date with Monica Lewinsky — are taken seriously because they tsk-tsk about deficits like Serious People™ and passively nod along whenever obvious liars are lying. This isn’t journalism. It’s Court Stenography, Versailles-on-the-Potomac.

Ain’t no use jiving. Ain’t no use joking. Everything is broken. So, no, I don’t feel particularly inclined to talk about politics these days either, because there’s only so many times you can bellow in rage about it all, especially when nobody swings by this little corner of the Internet anyway. I’m not officially quitting GitM or anything, but let’s be honest. I’m not really what sure when, if ever, it’ll get its groove back. I’m not sure I see the point. And besides, as Richard said, a withdrawal in disgust is not the same as apathy.

“The contrast in fortunes between those on top of the economic heap and those buried in the rubble couldn’t be starker. The 10 biggest banks now control more than three-quarters of the country’s banking assets. Profits have bounced back, while compensation at publicly traded Wall Street firms hit a record $135 billion in 2010. Meanwhile, more than 24 million Americans are out of work or can’t find full-time work, and nearly $9 trillion in household wealth has vanished. There seems to be no correlation between who drove the crisis and who is paying the price.“

“Lloyd Blankfein went to Washington and testified under oath that Goldman Sachs didn’t make a massive short bet and didn’t bet against its clients. The Levin report proves that Goldman spent the whole summer of 2007 riding a ‘big short’ and took a multibillion-dollar bet against its clients, a bet that incidentally made them enormous profits. Are we all missing something? Is there some different and higher standard of triple- and quadruple-lying that applies to bank CEOs but not to baseball players?“

“To recap: Goldman, to get $1.2 billion in crap off its books, dumps a huge lot of deadly mortgages on its clients, lies about where that crap came from and claims it believes in the product even as it’s betting $2 billion against it. When its victims try to run out of the burning house, Goldman stands in the doorway, blasts them all with gasoline before they can escape, and then has the balls to send a bill overcharging its victims for the pleasure of getting fried.”

“‘There can be no conceivable justification for requiring a soldier to surrender all his clothing, remain naked in his cell for seven hours, and then stand at attention the subsequent morning,’ he wrote. ‘This treatment is even more degrading considering that Pfc. Manning is being monitored — both by direct observation and by video — at all times.‘”

The president, meanwhile, assures us everything is ok because the Pentagon said so: “I have actually asked the Pentagon whether or not the procedures that have been taken in terms of his confinement are appropriate and are meeting our basic standards. They assure me that they are.” This, as Glenn Greenwald (who’s been on top of this all the way) points out, is exactly the same rationale Dubya used to use: “‘When [Bush] asked ‘the most senior legal officers in the U.S. government’ to review interrogation methods, ‘they assured me they did not constitute torture.’” Well, ok then.

Should Manning be in U.S. custody right now? Yes. He took an oath to the United States military and, knowing full well the consequences, broke it in an act of civil disobedience. If you can’t do the time, don’t do the crime — I get that. But should Manning be abused and tortured in U.S. custody? Of course not — Nobody should be. In fact, I thought we elected Barack Obama as president to make sure this never happened again.

Update: “Based on 30 years of government experience, if you have to explain why a guy is standing naked in the middle of a jail cell, you have a policy in need of urgent review.” P.J. Crowley reflects on his recent firing. “I stand by what I said. The United States should set the global standard for treatment of its citizens – and then exceed it. It is what the world expects of us. It is what we should expect of ourselves.“

“We had this gradual discovery during Hurricane Katrina, where a natural disaster eventually became seen as what it was, a man-made failure. And now, what was called an ‘act of God’ and a freak accident by the defenders of the pollution industry is now being labeled, proof positive, as the consequence of design failure. Not only did the blowout preventer under the Deepwater Horizon well have a leak in it, not only did it include a dead battery, not only were the tests on it falsified for years, but when engineers actually needed to use it and tried to activate it, they didn’t have the right schematics.“

As the Gulf runs black, it’s the same old story: FDL’s David Dayen brings us up-to-date on the idiotic and/or corrupt shenanigans coming to light in the wake of the (still-gushing) Deepwater Horizon gusher. “This is all a consequence of aggressive deregulation by industry, the maneuvers whereby powerful interests save billions in safety costs. They follow the rules at their discretion, they practically own the regulatory agency. It’s amazing how much this mirrors the problems on Wall Street. And just like with Goldman Sachs, the criminal justice system may get involved.” (Pic via TBP.)

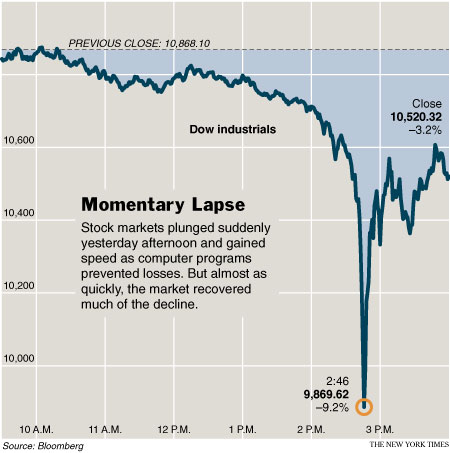

“The initial reaction of traders to the Flash Crash was that some human must have made a mistake submitting a trade. But the SEC…hasn’t found evidence of a ‘Fat Fingered Louie’ punching a billion rather than a million on an order. In fact, the SEC still doesn’t know what caused this crash. Curiously, no one is focusing on what caused the crash to stop…JP Morgan and Merrill Lynch were big buyers precisely as the market hit minus one thousand points on the Dow. It seems rather odd that both these firms at the same time would see the same trading opportunity.

In fact, what they did was violate one of the prime rules of trading: never try to catch a falling knife. The market was falling fast and furious at the point they entered the pit to buy equity futures, so why did they take such an enormous risk? We learned yesterday that both of these firms, plus Goldman Sachs, were such superb traders in the market that none of them had a single losing trading day all last quarter. This type of risky trade is not how you get to be a superb trader.

“

Over at the Agonist, Numerian digs deep into last week’s “Flash Crash” — and comes to some very troubling conclusions. To wit, the big players know the thresholds where the trading algorithms kick in, and thus, basically, the fix is in. “The stock market seems to be nothing but a playground for the big banks and other connected firms who get a preview peek at everything that goes through the market, and who can program their computers to skim profits off daily with no risk whatever. The stock market is also, quite possibly, prone to more serious manipulation that resulted in last Thursday’s crash.“

Oof. I’m out of my comfort zone when it comes to understanding market behavior, so I hope someone has a better explanation for the Flash Crash than the disconcertingly plausible one offered here. (Just saying Greece doesn’t quite cut it, I don’t think.)

“The big U.S. banks were the source of the global financial crisis, in part because their bigness and their practices were copied by major banks around the world. What happens in this reform effort is being watched avidly in many countries, because it will say much about how global finance is to be conducted. What is often missing in these discussions are the assumptions people make about banking and its role in a modern economy. We should begin therefore with some first principles.“

“Unfortunately, there are some in the financial industry who are misreading this moment. Instead of learning the lessons of Lehman and the crisis from which we are still recovering, they are choosing to ignore them. They do so not just at their own peril, but at our nation’s. So I want them to hear my words: We will not go back to the days of reckless behavior and unchecked excess at the heart of this crisis, where too many were motivated only by the appetite for quick kills and bloated bonuses. Those on Wall Street cannot resume taking risks without regard for consequences, and expect that next time, American taxpayers will be there to break their fall.“

But — see also health care — some wonder if the President is going far enough: “The problem with concentrating on the banking system is that it allows the administration to present an overly optimistic assessment of its actions…Taking credit for stabilizing the financial system after feeding it with massive amounts of federal money is like a teacher bragging about turning around the academic performance of a failing student after handing them all the answers to the big tests.“

Continues economist Nomi Prins, in an analysis that dovetails quite tellingly with the health-care situation:”A strong CFPA is a sensible plan…This proposal has drawn the most ire from the banking community, so you know it’s good…But Obama’s reforms do not strike deeply enough. The banking crisis has been subdued, not fixed, because of enormous amounts of government assistance. Ignoring that fact, and failing to overhaul the sector, leaves us open to another crisis. And the next round will be worse, because there is now so much more federal money invested in the banks.”